Postwar Art Remains the Auction Market’s Anchor

Early New Zealand sales declined sharply in 2025

This analysis is drawn from my 2025 New Zealand Art Auction Market Report. A comprehensive, data-driven review of the year’s key results, trends, and pricing signals. What follows is an extended excerpt highlighting the works that most dramatically exceeded expectations. You can download the full report below.

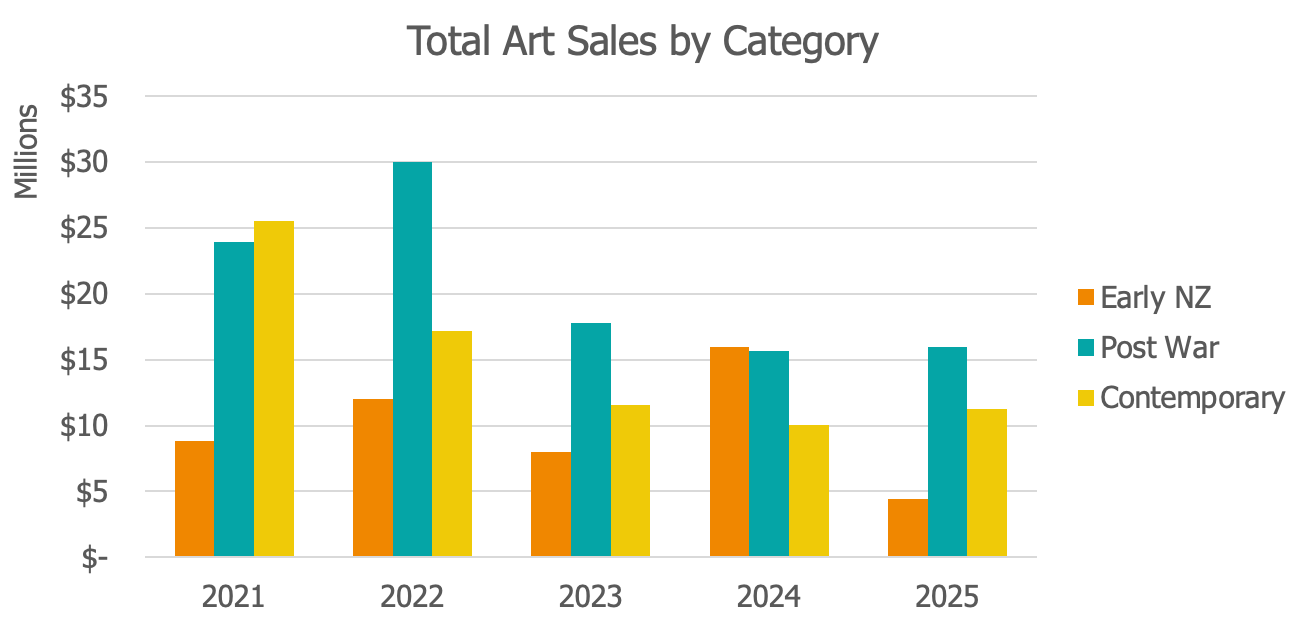

How did different generations of New Zealand artists perform in 2025? Segmenting the market by birth year reveals interesting structural differences in demand, concentration, and volatility. Some categories remain anchors of stability. Others are narrower or still forming. I’ve loosely followed Artnet’s grouping of categories by birth year.

Postwar (1911–1944)

Postwar artists continued to be the most lucrative and consistent segment of the New Zealand auction market in 2025. The category generated just under $16 million in sales, a modest 2% increase on 2024, and has remained broadly stable over the past three years. This segment includes many of New Zealand’s most bankable artists including Colin McCahon, Don Binney, Ralph Hotere, Tony Fomison, and Gordon Walters, and accounted for seven of the ten most expensive works sold during the year. It also delivered the strongest sell-through performance, averaging around 72% over the past three years.

This consistency reflects depth. Collectors continue to return to recognisable, institutionally validated artists from this mid-century cohort. A number of significant figures sit just outside the strict date range, such as Rita Angus (1908) and Bill Hammond (1947), which only reinforces how structurally strong this broader Postwar segment remains.

Early New Zealand (pre-1911)

By contrast, the Early New Zealand category experienced a sharp decline in 2025. This contraction was driven almost entirely by Charles F. Goldie. While 2024 had been an exceptional year, with Goldie’s works generating nearly $12 million in sales, results in 2025 fell to under $1 million as the market absorbed that unusually strong prior year. Despite this volatility, sell-through rates for the category have remained relatively stable, averaging around 69% over the past three years.

The category’s challenge is concentration. A small number of artists drive the majority of value, with Goldie dominant alongside Gottfried Lindauer and Frances Hodgkins. Without results from these three artists, overall results are materially affected.

Contemporary (1945+)

Sales for Contemporary artists were broadly stable over the same period. In 2025, the category recorded a small uplift, supported by stronger results for artists including Karl Maughan, Shane Cotton, Grahame Sydney, and Brent Wong. However, Contemporary works remained underrepresented at the very top end of the market, with only two works appearing in the top 20 most expensive sales of the year. Sell-through rates for Contemporary art have been consistently lower than Postwar, averaging around 65% over the past three years.

Contemporary remains the most volatile segment, with total sales still less than half the 2021 pandemic spike. That is not necessarily a weakness. This is a market still forming. As new leaders emerge and price ceilings are tested, today’s contemporary artists may become tomorrow’s blue-chip anchors. For now, it remains the most dynamic and arguably the most interesting segment to watch.

Taken together, the data shows a market behaving differently across generations. Stability sits in the mid-century names, concentration defines the earliest works, and contemporary remains more fluid. Those distinctions help explain many of the year’s headline results.

Note: Approximately 3% of sales did not have an artist birth date recorded and have been excluded from this analysis.