Women Breaking Records, Not Yet Barriers

Women artists delivered some of the standout auction results of 2025, but structural underrepresentation still defines the market in Australia and New Zealand.

This analysis draws on my 2025 reports on the fine art auction markets in Australia and New Zealand. Those reports provide a data-driven review of the year’s key results, trends, and pricing signals. What follows is a closer look at how women artists were represented in those markets in 2025, and where the strongest gains and the clearest gaps remain.

2025 New Zealand Market Report | 2025 Australia Market Report

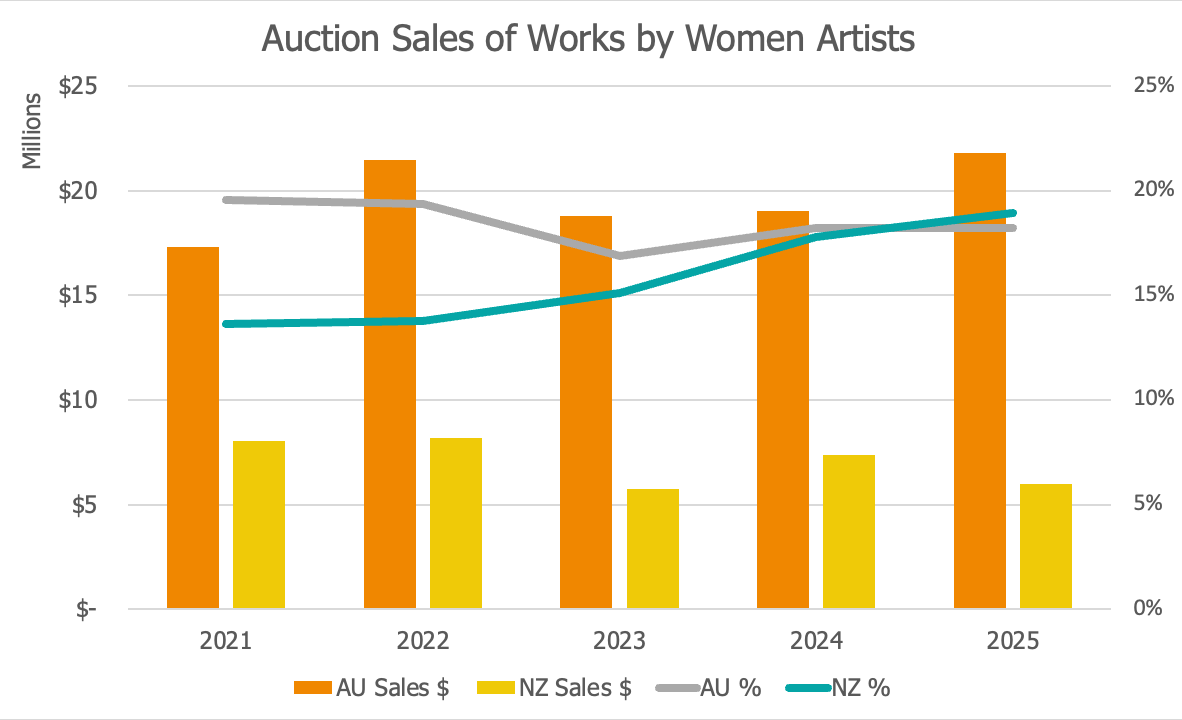

Women artists remain underrepresented in both the Australian and New Zealand auction markets, but 2025 offered some meaningful signs of progress. In Australia, works by women accounted for 18.2% of total sales value, broadly flat relative to recent years. In New Zealand, female artists accounted for approximately 19% of total auction sales value, up from 14% in 2021. Record prices and stronger mid-market representation suggest momentum is building, even if from a relatively low base.

Note: Sales have not been adjusted for currency. In practical terms, that means Australian sales are even higher relative to New Zealand than what’s depicted in the graph.

Headline Results

Despite women’s relatively modest overall market share, 2025 still delivered several major record-setting results.

In Australia, Emily Kame Kngwarreye became just the fourth female artist to have a work sell for more than $1 million AUD at auction, when Untitled (Awelye) sold at Deutscher and Hackett, also setting a new record for the artist. A new auction record was also set for Grace Cossington Smith with The Reader (The School Cape), which sold for just under $1 million AUD, also at Deutscher and Hackett. Both works now sit among the ten most expensive auction results for works by Australian women artists. Another record result came from Dorrit Black, whose Sicilian Mountain sold for $687,500 AUD at Smith & Singer, setting a new record for the artist.

New Zealand also produced an important milestone with the sale of Rita Angus’ Before the Demolition, which achieved $621,435 NZD at Art & Object. It was the second-highest price of the year overall, and notably the second-highest auction result ever for a female artist in New Zealand, with Angus also holding the national record. The next-highest result for a New Zealand woman was Louise Henderson’s Setting Sun Indian Ocean, which sold for $143,400 NZD at Webb’s. That is a strong result by New Zealand standards, but it still ranked only 36th in the New Zealand market by price in 2025.

Taken together, these results underline an important point: record prices are being set, but progress at the top remains concentrated. A small number of exceptional works can create the impression of rapid change, even when the wider market structure remains much the same.

Better progress in the mid and lower tiers

The clearest gains were not at the very top of the market, but further down the price ladder.

In Australia, women have accounted for roughly 11% of sales value above $500,000 AUD over the past five years. That improved to 14% in 2025, helped by the headline results noted above, but still below the overall figure of 18.2%. Representation has been strongest in the $100,000–$300,000 AUD range, averaging around 26% over the past five years, though easing to 23% in 2025.

New Zealand shows a similar pattern. Representation above $100,000 NZD remains limited, with women accounting for around 8% of value in that tier over the past five years, with little change overall. By contrast, gains have been stronger below the six-figure level, where women accounted for 26% of sales under $100,000 in 2025, up from 19% in 2021. Sell-through rates for female artists also improved to approximately 68%, marginally above those for male artists.

That is perhaps the most encouraging part of the picture. While the very top end remains stubbornly male-dominated, women are gaining ground across much of the middle market, where depth of demand matters more than a handful of standout trophy works.

Stronger representation in Contemporary art

Women continue to be better represented in Contemporary art than in other categories, although even there progress is uneven.

In Australia, four of the top ten selling Contemporary artists in 2025 were women, although that falls to 28% across the top 50. New Zealand shows a similar pattern: women perform better in Contemporary art than in other categories, but only two of the top ten Contemporary artists were female, even though women made up 30% of the top 50. In other words, there’s still room at the top end for New Zealand to catch up with Australia.

Photography may also be emerging as an especially important female-led segment in New Zealand. Marti Friedlander continues to perform strongly at auction, while Fiona Pardington entered 2025 with major institutional momentum after being selected to represent Aotearoa New Zealand at the 2026 Venice Biennale. That kind of institutional recognition does not always translate directly into auction results, but it can strengthen visibility, confidence, and long-term market attention.

Where some of that progress is coming from

In New Zealand, part of the improvement may reflect not only changing collector demand, but also a changing approach from auction houses, galleries and museums. International Art Centre’s dedicated Women in Art sales have helped bring greater visibility to female artists and have contributed to new records for artists including Star Gossage, Pauline Yearbury, Marti Friedlander, Flora Scales, Kushana Bush, and Evelyn Page.

That matters because markets do not shift only through demand; they also shift through curation, supply, and the confidence created when artists are deliberately foregrounded.

There have also been a revival in female focused exhibitions across public galleries, including Auckland Art Gallery’s significant exhibition of women artists with Modern Women: Flight of Time, as well as the Dunedin Public Art Gallery exhibition of Groundbreakers: Grace Joel, Frances Hodgkins and the new art of Ōtepoti, both in 2024.

This is worth emphasising because it suggests that auction representation is not just a passive reflection of the market. It can also be shaped by the way our auction houses, commercial and public museums choose to frame, group, and promote artists. In that sense, 2025 may point not only to stronger demand for women artists, but also to more active market-making around them.

Artists to watch

Beyond the headline records, several women artists continue to show increasing demand in the secondary market.

In Australia, Bronwyn Oliver, Margaret Olley, Criss Canning, Florence Fuller, Inge King, and Carol Jerrems all stand out. Some are benefiting from sustained collector demand, while others appear to be gaining ground through renewed historical attention and record-setting results. Olley set a new auction record in 2025, while Jerrems also saw a major record for her landmark photograph Vale Street.

In New Zealand, artists such as Robyn Kahukiwa, Jenny Doležel, Pauline Yearbury, Star Gossage, Lisa Reihana, Dorothy Kate Richmond, Marti Friedlander, Evelyn Page, Flora Scales, and Fiona Pardington are all worth watching. Some are already well established, while others are benefiting from more consistent auction visibility or a growing market reassessment of their importance.

Conclusion

Overall, 2025 reinforced a familiar pattern. Women artists are gaining visibility, setting new records, and improving their position across much of the middle market. But the structure of both auction markets remains largely unchanged. Progress is real, yet it is still concentrated, uneven, and far from complete.

At the top end especially, underrepresentation remains persistent. The more encouraging story lies below that level: a broader pool of women artists is finding support, sell-through rates are improving, and both institutional and commercial attention appear to be widening. That is not the same thing as parity, but it is how markets begin to change.

Note: Approximately 1% of Australian sales and 3% of New Zealand sales did not have artist gender recorded and have been excluded from this analysis.